There's been no lack of financial news since

my last finpost when Hindenburg exposed Adani and Burry tweeted some technials and then, simply, "Sell". Sneak peak:

- JPow vs inflation

- "The 0DTE craze"

- Check back on /u/Retire-early2 in a few months

- Banks and JPow vs inflation

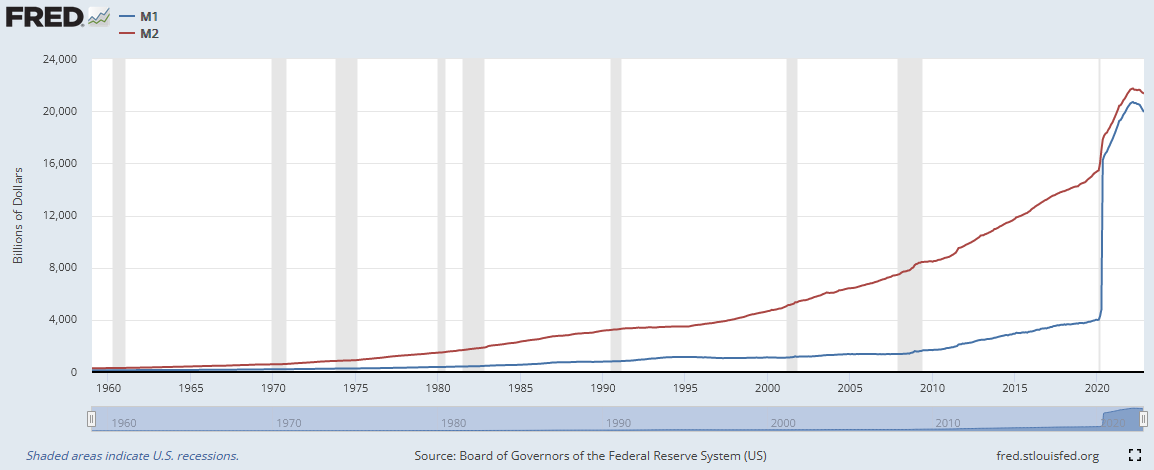

Inflation and taxation

The main economic plotline for 2020-202x is

the Federal Reserve fighting the inflation it created with years of low interest rates and 2020's monetary policy. Sure, supply chain issues and war played a role, but the money printer most assuredly went brrr.

Inflation is the main economic plotline for 2020-202x, right?

Or is it the national debt that also exploded during the pandemic? Either way, we have two big post-covid problems.

Post-reappointment

JPow has been hawkish about inflation. The Fed is going full steam toward terminal interest rates around 6% while talking heads claim they see a pivot in the tea leaves. Powell's stated goal is to use interest rates to cool spending, increase unemployment, and thereby tame inflation. It goes without saying that unemployment is socially painful and increases the burden on public resources.

Last year I read

some stuff about people borrowing against riskier (portfolio) and more stable (home) assets. So this anecdote was alarming:

|

/u/atr1ll

What I learned as a Banker doing tons of Helocs and cash out Refis and going into second positions is as Americans we love to buy stupid stuff. Boats, Cars, and other houses. If you obtained a heloc in 2020-2021 with 4 percent rates those floating rates are killing people as we speak you went from paying a thousand to now paying two thousand a month. As we have seen credit card debt explode to a trillion dollars, car loans being defaulted and student loans needing to be repaid around in September. Housing will not burst the bubble it's people's lifestyles and needing to be maintained for that "image"? These types of reports of everyone refinanced in 2020 or 2021 is a misnomer of what truly underlies is we have a spending problem and it will be too late unless everyone just stops spending money and living by their means. I just realize we have a bunch of idiots that don't know how to spend their money. I am not a bear on housing but actually see and deal with a ton of people everyday. Look up EIDL loans for small business and see that ticking time bomb.

|

|

|

/u/woody1594

Yep. Started my heloc at 4 percent and it's currently at 8.5 percent. Luckily I've only used 20k for a new roof and some new windows. But it's still eye opening going from 70 dollars interest a month to 175 interest a month. Must be killing people that took out 100k + for a rental house or just stupid spending.

|

Reducing spending

I think if I had read a macroeconomics textbook recently this would have been obvious. But I get a little bit of Marketplace and a little bit of WSB and have a lot of time to contemplate what I've heard/read. Since I'm probably not the only one in this boat, I'll say this with a only modicum of shame: it seems like

there's a better way to decrease consumer spending but also address the debt/deficit issue. One that is strangely absent from The Conversation. I found the suggestion on

/r/economics:

|

|

/u/NateDawg007

I have wondered why there has been basically zero discussion of raising taxes. Increased taxes combined with lowering the deficit or better paying off debt also lowers the money supply. Lowering the debt is also good so that in a deflationary environment, we can increase the debt more easily because we have paid it down.

|

|

|

|

/u/pmac_red

> I have wondered why there has been basically zero discussion of raising taxes.

Voters don't reward politicians who do.

|

Right?

Tax hikes address the deficit/debt issue while also achieving JPow's goal of decreasing spending. Tax increases aren't free of consequence, but they're a more evenly-shared burden than inducing layoffs.

I wonder if that's why (based on what NPR told me), when Elizabeth Warren recently asked JPow if he thought about the people losing their jobs he testily responded with something like, "Would they be better off if we just walked away?" Perhaps he didn't want to be criticized, perhaps he is unhappy with this limited set of monetary tools. But

perhaps his ire bore the additional subtext, "You have it in your power to help fix this with something more effective than a spending bill marketed as de-inflationary".

Economics is all give and take, so I don't want to talk up tax hikes like its a golden hammer, but it's disappointing that it's not the first suggestion in every conversation.

|

/u/jr1tn

Wouldn't the Democrat Biden administration just appoint a more Keynsian candidate? Dovish not hawkish?

|

|

|

/u/thatguy201717

They have to crush inflation this year...you can't go into a presidential year with inflation still being high. Jpow will have to take fed fund rates to 5.5% this year which will cause a recession. Cut rates in early 2024 and economy should be roaring back by summer 2024 heading into the final months of presidential campaign

|

|

|

|

/u/GayPerry_86

They have to crush inflation because structural inflation will develop. We can't have major corporations and small businesses expecting 6% inflation regularly, and once these numbers get incorporated into budgetary projections, it becomes structural and self-fulfilling.

|

All the talk of

positive feedback with inflation gives me the heebie-jeebies.

notthebestchristian notthebestchristian |

Fuck my life, the COVID bailouts were just another massive bailout for the business class paid for by the American taxpayer, the taxpayer's children, and grandchildren.

They're simultaneously robbing every American's retirement fund and their home value, the single largest value store most Americans have. Now in the name of "combating inflation" they're artificially destroying home and stock values so the rich can swoop in and grab them at a discount.

|

Imagine my surprise when we elect the ostensibly wealthy guy who wants to run the government like a business but then he turns around and helps the wealthy and businesses over everyone else.

0DTEs

attofreak attofreak |

[The Big Short] and Wolf of Wallstreet was made for us gambling degenerates pretending to "invest". It's like Fight Club, but for pudgy, lazy guys who think clicking on a button furiously counts as aggressive combat.

|

Financial news had

a brief panic about the rise of 0DTEs. It's somewhat surprising that this was noticed long after the

GME saga.

The Economist

The Economist |

Not long ago trading in American stock options was limited mainly to professional investors. Options are contracts that provide the right to buy or sell a security at a specified price over a fixed time period. They can deliver big payouts if a stock moves in the desired direction, and expire worthless otherwise. Sophisticated buyers use options to hedge against risk, generate income or as a form of leverage. However, options can also be used to gamble.

Interest in American options has grown rapidly since the covid-19 pandemic began. In early 2020 the number of options traded per day rose from 20m to 30m. It surged again to 40m in early 2021, when trading erupted in "meme" stocks such as GameStop and enthusiasts flocked to options to magnify their bets. Trading has reached record highs this year. The average in February was 45m, and on February 2nd 68m contracts changed hands.

...

Moreover, rather than trading options that last for weeks, months or years, buyers are now piling into zero-days-to-expiration (0dte) contracts. These options, which expire the day that they are bought and yield windfalls if a price moves sharply that day, became more widely available in 2022, after exchanges increased the number of trading days on which they are available. As meme-stock mania has faded, 0dte options, mainly written on market-wide indices, have become the new fad. Daily trading of 0dte contracts recently reached a record notional value of $1trn.

...

Even if options do not threaten markets as a whole, they clearly represent a siren song for retail investors. Despite the rise in share prices since early 2020, traders who have treated stockmarkets like a casino have on average fared about as well as a typical slot-machine player. The Journal of Finance authors estimate that between November 2019 and June 2021, retail investors collectively lost $2.1bn on options.

|

An old school yolo

Like I

said a few days ago, WSB has changed over the last couple of years but its spirit is not gone (unless OP is paper trading). A huge Roth IRA bet on a leveraged commodity ETF is just as ballsy as a SPY FD. But I digress, the reason I found this post worth mentioning was for one of the comments:

|

/u/Retire-early2

Thanks - no calls/puts in my retirement accounts are allowed so I use the 2-3x etfs. People say the 'fee' decays the fund. It's really a minuscule amount they take over time. Around 1% annually I think. I've never even noticed decay tbh.

|

|

|

/u/Undercover_in_SF

It's not the fee, it's roll and volatility decay. These things are terrible to own for more than a few months. Look at any long term chart of KOLD or BOIL. They've done reverse splits to keep the price above $1.

So what are roll losses? Well, these ETFs don't own the physical commodity. They own futures contracts. BOIL and KOLD in particular own March, June, September, and December futures. Every 3 months they sell the current contract and buy the futures contract. But futures don't predict the underlying. Usually they're overpriced or in what's called contango. You don't lose the delta between the two contracts immediately, but as the overpriced futures contract falls to meet the commodity price, the value of the ETF underperforms the commodity.

What about volatility decay? These funds use leverage to track 2x the daily return of the index. If the index falls 10%, BOIL should fall by 20%. The index now has to go up by ~11% to get back to the prior price, but BOIL has to go up by 25% to get back to its original value (100x80%=80; 80x125%=100). But the index isn't going to keep going up forever. If it just goes back to the original price then BOIL goes up 22%. 80x122%=97.6. Your ETF just lost 2.4% because it's only designed to track daily movement.

I don't really expect you to read that or care. You're clearly in the right place. So good luck! I hope you get rich, but the odds are against you.

|

I cautiously

agree with OP that energy is a reasonable investment in this kanga-bear market, but a leveraged ETF seems unwise here. I just wish this thing would crash already so we can start buying again.

mjkjg2 mjkjg2 |

if I had $3.8 mil to make a single trade with, I'd buy SPY shares and sell covered calls or some dividend ETF that pays like 2% monthly, that's $80k per month

|

Selling weekly SPX covered calls is the dream. But buying into SPX at $4,000 and watching it decline to $3,000 would be a nightmare.

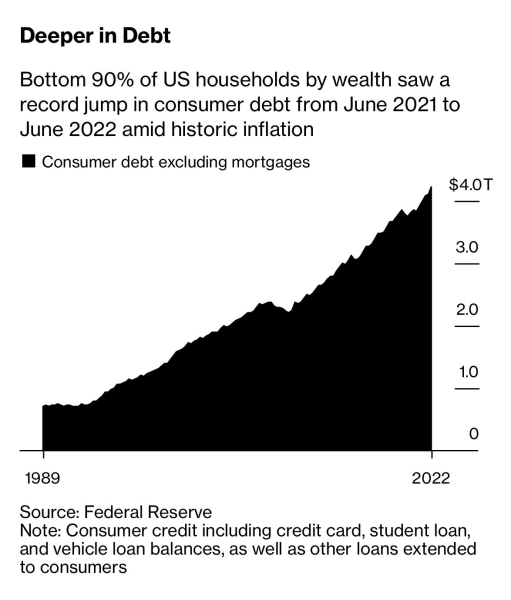

Consumer debt crisis

|

|

|

There have been a lot of charts like these recently though they're rarely per-capita or inflation-adjusted. |

|

|

/u/SirLeaf

It is, on paper this is a massive win for creditors.

|

|

|

|

/u/Expensive_Web_8534

I, too, like to be holding fixed rate instruments while the rates are rising. I finally feel like I've found home.

|

Speaking of fixed-rate instruments and rising benchmark rates...

Banking crisis

- SVB: the Fed took over the bank after it couldn't cover withdrawals. There is a delicious rumor that someone organized a bank run, but the word is they got into their liquidity mess by holding a lot of underwater bonds.

- Signature: the tldr seems to be that this is FTX fallout.

- Credit Suisse: speculation about Credit Suisse has swirled since they were left holding the Archegos bag.

Here's an uplifting thing I read: the reserve requirements and

stress tests imposed by Dodd-Frank were lifted during the last administration, but not for megabanks like BofA and Wells. If anything, troubled times for regional banks seems like an opportunity for the big boys to get assets on the cheap. Maybe if a ton of regional banks go down there'll cause for concern, otherwise it just as well that the Fed pledged to cover depositors' money.

Treasury and the Fed were quick to assert that the SVB takeover would be funded by bank FDIC fees, not taxpayers.

So, all's well?

All may not be well. After the SVB and Signature thing, First Republic's share price plunged 50% in a couple of days. More bank whack-a-mole for Powell and Yellen? Apparently not, a bunch of big banks poured money into First Republic in a weird showing of solidarity amongst frenemies.

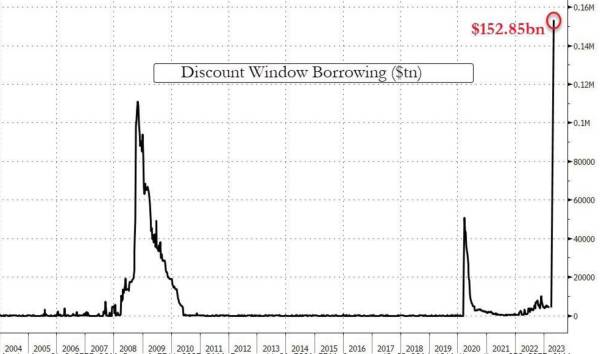

Bailouts, repo, and FDIC insurance

|

|

Source. I tried to find the chart on the St. Louis Fed site, but couldn't, so here's the one from WSB. As noted in the comments, this isn't scaled to money supply. |

For context, when a bank needs short term liquidity, it can borrow from other banks or from the Federal Reserve's repo program or discount window. It's a neat mechanism to allow banks to make more money by operating with lower reserves.

|

/u/fuerstjh

Real question...how many banks are just taking this money cuz it's cheap even if they are not at any liquidity risk?

If the government showed up at your door today and said "oh hey ill give you a loan for 1% interest" what would u do?

|

|

|

/u/Happyfunball222

I work in banking/finance and that's exactly what we did lol. It was referred to internally as a Trojan horse

|

|

|

|

/u/sonkist32

Nobody gets it. Let them borrow at 1% they will just turn around and buy a 1 year tbill at 5% and make a 4% arbitrage for a year. Literally free money lol

|

WSB had

1,

2,

3 posts about the

$300B spike in the Fed's balance sheet and a

fourth about the discount window borrowing (which I assume accounts for half of that balance sheet increase). Alas, I couldn't find much more info from WSB or /r/economics or the major financial news outlets.

The pessimist's view is that a bunch of regional banks are having a Lehman moment and suddenly pounding on the Fed's door. I don't think that balance sheet number has enough 0s to represent a systemwide liquidity problem, but let's give it time.

|

Axios |

Banks also had $12 billion in credit from the Bank Term Funding Program, announced Sunday night, to make bank lending available on highly favorable terms. The report does not say which (or how many) banks tapped the facility and won't do so for another year.

|

Alternatively, /u/Happyfunball222's view is that banks saw JPow dusting off the money printer and saw an arbitrage opportunity. So they'd be basically be trading progress against inflation for a few percent return on $12B.

|

CNN |

Treasury Secretary Janet Yellen on Thursday met privately in Washington with JPMorgan CEO Jamie Dimon before 11 banks agreed to deposit $30 billion in First Republic Bank to stabilize the teetering lender, according to two people familiar with the matter.

|

"Hey guys, if you each put $3B into First Republic to make it look like a private sector bailout, we'll let you tap the $12B liquidity facility meant for struggling banks."

Outlook

|

Everyone, ever |

Don't fight the Fed.

|

Until we hit JPow's target interest rates

money will be sucked out of the markets and any good stonks will be fighting and uphill battle. There may be a few bumps along the way if any of the risks (bank failures, consumer debt, commerical real estate, Ukraine escalation) turn into problems.

Some posts from this site with similar content.

(and some select mainstream web). I haven't personally looked at them or checked them for quality, decency, or sanity. None of these links are promoted, sponsored, or affiliated with this site. For more information, see

.

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/01/stellaris_event.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/07/warrior.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/01/_CRR2781.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2019/01/viscera_cleanup_mop.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/01/elon_birb.png){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/02/far_cry_view_00.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/01/_CRR2726.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2017/05/dying_light_stadium.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/01/tongue.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2016/04/division_helo_00.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/01/27_dresses.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2020/09/da_bears.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/01/_CRR2878.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/11/deezer.jpg){kind=link}