Finpost:

- Soft landing or ______ meltdown?

- How to lose money with a 5% yearly interest payment

- Wheeling TLT and terminal rates

- Buy-write ETFs, finally

Hindenburg Omen

Since

Cattle likes to use

Hindenburg Omen (and ad hoc variations thereof) as shorthand for

technical analysis ͥ , it was on the tip of my tongue as I reviewed my backlog of financial news. Since

much of this news is 'crash incoming', it seemed like an apt title, even though I'm not expecting a repeat of

September 29 any time soon.

There is

plenty of reason to believe in a non-catastrophic market pullback, I

previously mentioned the chorus of CEOs that predicted a late-2023 economic downturn. Interest rates are up and the real estate lobby is begging the FED to reverse, China isn't growing anymore, nobody cares about the next iphone or Galaxy, and there's massive debt hiding under every rock in the economy. So I'm thinking the moves are cash, inverse ETFs, and energy. Others might take short positions, buy puts, and invest in consumer defensive. With the decay associated with short positions, I've found it tough to find a good bear market strategy.

Black swans

|

|

|

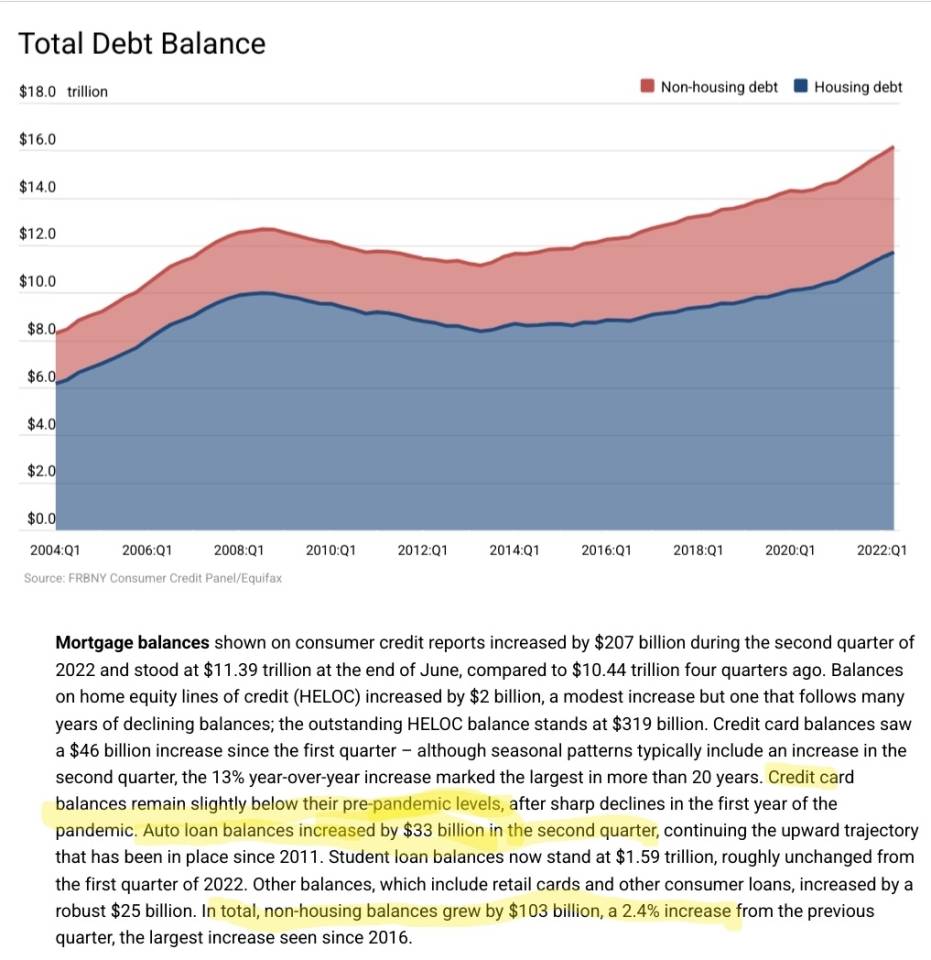

Considering inflation, we seem to have actually gotten better with credit cards. |

Slow decline? Boring. More exciting: "

everyone is going to default on their 96-month auto loans, the repossessed cars will not cover the balance, the lenders will go bankrupt, and the dominos will keep falling". In the next breath, "but if you buy gold..."

I don't buy it. The pandemic was supposed to destroy the global economy but we printed our way out of it.

SVB and company were supposed to bring the banking system to its knees but the Federal Reserve handed that rather deftly.

The DoJ seems to be making an example of SBF, so the Jeff Skillings and Bill Hwangs of the financial system are officially on notice. It's hard to buy into any "imminent black swan", but they're fun to read about.

Fortune

Fortune |

"We are in the greatest credit bubble in human history. And that's not my opinion, that's just numbers," he said. "There is no question about the fact that we are living in an age of leverage, an age of credit, and it will have its consequences."

To his point, total U.S. household debt hit a record $17 trillion in the first quarter, New York Fed data shows. And global public debt surged to an all-time high of $92 trillion last year, a 400% increase since 2000, according to a United Nations report released this month.

|

Place your wagers on

the cause of the next global financial crisis...

- Consumer debt

- Commercial real estate and/or commercial mortgage-backed securities (2008 but with offices and strip malls)

- China property collapse (Evergrande, Country Garden, ponzi-ish structure systemwide)

- Yield curves crossing or double crossing or triple axling or whatever

- Banks having too many 1.5% treasurys and nobody wanting to buy them because new ones are 5%

- The Supreme Court rules the Federal Reserve unconstitutional (with other institutions not funded through appropriations)

- An invasion of Poland, Taiwan, Iran, ...

Bonds, bond funds, and a 401k

|

|

|

Timing the market > time in the market. |

With that vague allusion to a bearish or risky investing environment, let's talk actual moves. One thing you can do when the major indexes are consistently red is

buy bonds. They pay interest, you don't have to do anything, and they only go to zero if the company goes bankrupt (at which point you're higher on the creditor food chain than shareholders). There are some ins and outs, but that's the gist of it.

I like bonds. I like my 7+% Ford and Safeway bonds because I don't expect the companies to go bankrupt, they pay me twice a year, and when the bonds mature I'll get their face value back. I also might sell them for a profit if their resale value gets high enough. In contrast, I've historically not traded bond equities (TIP and TLT and IEF). They pay a variable dividend and fluctuate in value, for that kind of action I'd rather trade something that moves more.

The glaring exception to this policy is my 401k where, like many, my retirement contributions go to one of a few dozen buckets. A little while ago I moved a bunch of my 401k money into the brokerage's low risk funds, trading some potential upside to avoid a repeat of 2008. My intent was to wait for the pullback and then go wild on SPX and QQQ and VTI.

It's a 401k, so I could afford to be patient and tolerate 5% annual gains + my contributions + employer match. It'd be considerably better than having another mortgage-backed securities disaster delete most of my retirement port.

My goal was temporarily limit downside but I admit

I came in with the expectation of extremely modest gains. Low risk funds are mostly bonds, who can't make small gains on bonds?

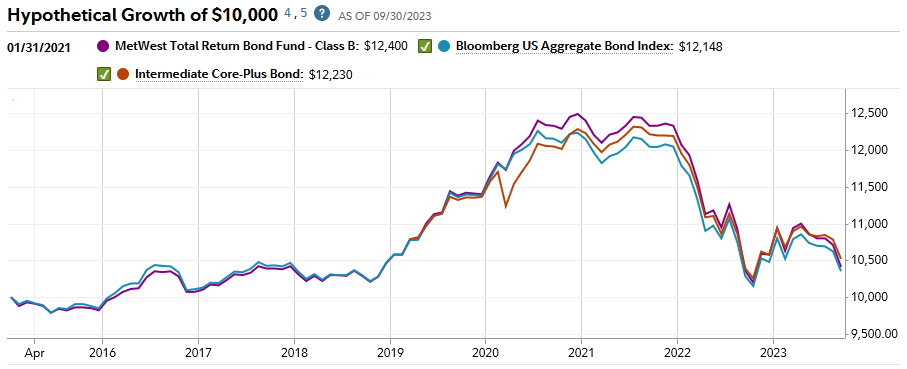

So I was pretty annoyed to find that

the ten-year performance of the MetWest Total Return Bond Fund was just about flat. In ten years it gained what a money market account would gain in a year. Anything I contributed before 2019 didn't go anywhere (see above) and anything I contributed during the pandemic lost value.

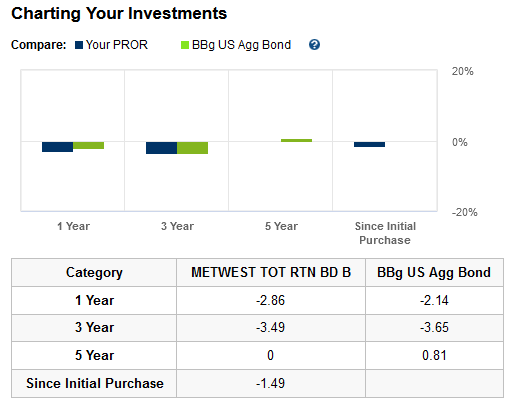

Wile I appreciate that

-2.86% in one year and -3.49% in three years is low risk (especially seeing only a small dip in spring 2020), I put money into a bond fund hoping it'd mirror the underlying instruments and return small, steady gains. How do you even lose money on bonds?

The answer to my rhetorical-sounding question is the same as

for any investment: "by buying high and selling low". ('Selling' isn't strictly accurate here because at the moment the losses are unrealized.) Interest rates were near zero for a full decade so bonds were expensive until the FED's inflation-taming rate hikes. Rates go up, values go down. And that's how you get the post-2021 drop in MetWest Total Return Bond Fund, probably.

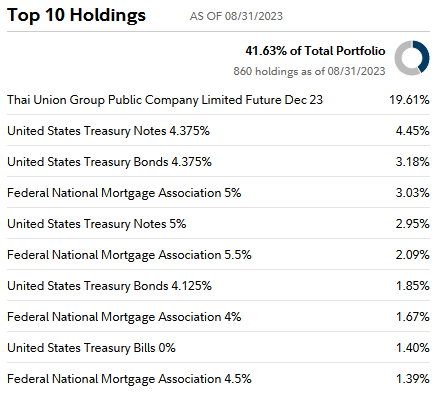

But look at all of those 4-5% bonds. The

interest payments on the fund's holdings seem to have been gobbled up by its retreating market value. I'm not sure why 20% of the holdings are a Thai seafood company, but maybe in Dec '23 there will be a big payout.

The smart thing would have been to

pull my funds out of MetWest Total Return Bond Fund when it became clear that the president and FED were planning to address the whole money printer/inflation issue. With limited 401k options, I didn't have many risk-averse alternatives, so ???

Brokeragelink

I don't really need MetWest. I can lose 3.5% of my retirement fund value on my own and I don't even need three years to do it. My 401k allows equities trading if you click a bunch of acknowledgments.

Since

I'm actually inclined to collect bond interest rather than have it disappear into some opaque fund, I can buy 7.75% senior notes from Ford Motor Company at almost par value. And in a few years when rates are low again, I'll be able to sell those notes for a tidy profit. Or hold them, because as Warren Buffet says, "compounding gains, amirite?"

Minor caveat: it turns out that I, in fact, need MetWest. Not because Ford is in danger of going bankrupt but because

Fidelity won't let me pull completely out of their stupid funds.

Jupman Jupman |

T-bonds are there to just beat the fact that you can't get shit in a basic savings account.

If you want good advice, call your broker's Bond Desk they have nothing to do, and no one calls them.

|

(Since this comment was written, basic savings accounts started offering like 4% interest, for now.)

One more reason I don't like 'Target Date 2045 Fund'

Again, I'm not expecting to see

Plunge Protection Team fastroping out of Black Hawks any time soon but having gotten into the 401k game in 2008 it's hard not to have my ears angled toward anything that sounds like catastrophe. From a 2021 post:

Me Me |

[The China Hustle documentary] mentions that retail traders took the biggest hit in the initial round of RTO (reverse takeover) fraud and that estimates for pension fund losses were $14B. I'm inclined to believe my 401k has exposure to this kind of thing. QQQ certainly does. And so I feel a renewed emphasis to DIY my portfolio diversity rather than let institutions wash away these losses behind a wall of opacity and "Well Moody's rated these mortgage-backed securities as investment-grade so it's not on us if they go tits up".

|

I am more than happy to have control over my investments.

Terminal rates

From WSB:

pareofdocks pareofdocks |

Let's say you have $93,000 sitting in a broker account. You should be getting 4.5-4.9% interest on it. If you want, you can sell December 15th TLT $93 puts for $3.05. Sell 10 contracts for $3050. By December 15th, your cash will earn you about $1450 in interest, and if TLT is above $93, you keep the put premium. You made $4500 in about 4 months, which is over 14% ROI annualized. If TLT is lower than 93, you have to buy it at 93 and get stuck with a treasury ETF which pays 4.3% per year. You can now sell calls against your shares and boost that 4.3% to something higher. You only lose if interest rates go up substantially higher, which is pretty unlikely.

|

As /u/Zaros262

points out, this is just

the wheel for an ETF that tracks the 20-year. Having wheeled NFLX and MSFT and OIH and NVDA, this interested me, so I did some homework in the comments section and elsewhere.

- While TSLA can bounce between $100 per share and $400 per share in six months, bonds don't move all that much. In two decades TLT has mostly swung between $80 and $120, though covid took it up to the $160s.

- The lack of volatility often means options premiums aren't all that great. Indeed, 3% for a three-month contract isn't much of a payout in thetaland.

- A month after the post, TLT is now below $85 so OP would be looking at owning 100k of TLT and taking that 4.3% per year.

devilsgospel666 devilsgospel666 |

If there's still upside to inflation (there is) and we get more hikes, could you sit with 100k in illiquid funds comfortably until rates are cut? Whenever that may be, with some expectations being years?

If you can by all means go for it, but as someone else said before, this method of options trading almost ensures you will have to win much much more than lose. A drawdown on the underlying could easily be more than your premium gained from several spins of The Wheel and then once again your funds are illiquid until rates come down. That's where shit like opportunity cost comes into play.

|

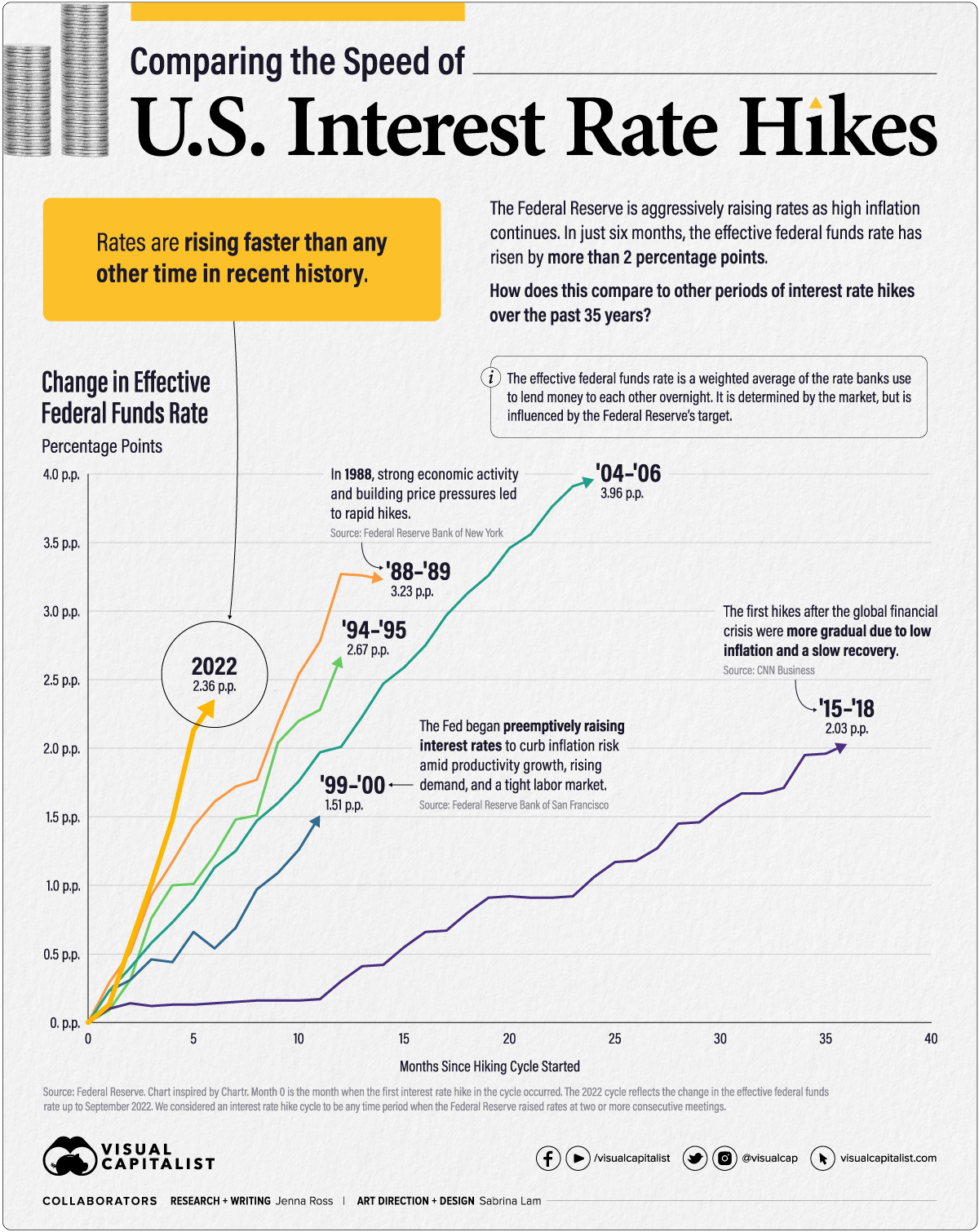

Since rates will go back down, TLT will eventually come back up, but there's a lot of opportunity cost lost to a position that comes in $9,500 increments. Since an

18-month hiking regime to get from 0% to 5% was

considered extremely quick,

I don't think the interest rate downslope will be difficult to time. But when cheap financing returns there will be more profitable places to put your money.

Stormranger_jj Stormranger_jj |

The pricing of options is calculated using a very complicated formula. I recommend googling "black-scholes formula." This formula isn't perfect however, so I believe market makers use variations of it to calculate options prices.

With this said stocks where big moves are expected tend to have high implied volatility. This is a key metric in calculating the pricing of options. In short, I imagine TLT is one of these stocks. Even if it may seem like there's a small chance that the puts OP sells doesn't expire worthless, there is a significant enough chance to warrant pricing the option high enough to give OP a 14% yield over the time of the investment.

Basically its like picking up pennies in front of a steam roller. With this strategy OP will likely get several wins at first, and a decent return. But one day a big downward move will happen in OP's underlying stock, wiping out all their returns.

The options market is priced relatively efficiently. If this strategy would've worked, a hedgefund or big bank would of discovered it by now, and eat up all the profits available from the inefficiency in pricing.

|

And so it did.

Quantitative tightening

|

Richmond FED |

When the COVID-19 pandemic hit the United States in early March 2020, the Fed quickly stepped in to limit the economic fallout. It reduced its interest rate target to near zero and purchased large quantities of U.S. Treasury bonds and mortgage-backed securities (MBS) by injecting reserves into the banking system. As a result of these purchases, the size of the Fed's balance sheet more than doubled from about $4 trillion prior to the pandemic to nearly $9 trillion at the start of 2022.

|

Since the Federal Reserve's

balance sheet is partially comprised of treasurys, their quantitative tightening regime probably means we have farther to go.

Putting it all together: theta gang ETF

I'm not sure the time is right for OP's TLT strategy, but I am on board with

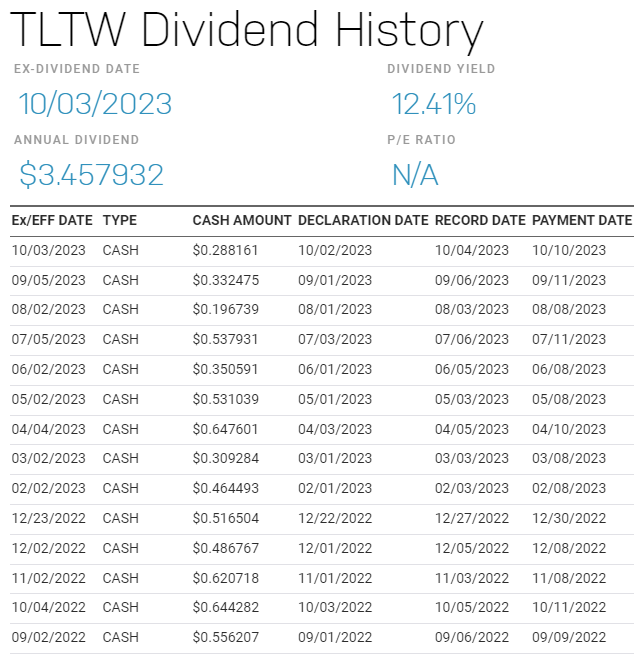

writing covered calls as a way to make weekly profit on a stock I'd already be holding anyway. And so I was interested to learn of TLTW,

20+ Year Treasury Bond Buywrite Strategy ETF.

|

BlackRock |

Last year, iShares launched the first ever ETFs to employ a bond ETF buy-write strategy, making it simple for all investors to add covered call strategies to their portfolios.

|

"But Chris, you just railed on bond funds because the interest payments go into the fund value, so you gain nothing until you sell." Not here:

|

|

Source. So 100 shares ($3,300) of TLTW paid $520 in dividends over the past year. |

Of course, like its underlier,

TLTW should decline until interest rates top out and QT is over.

|

|

Source. Those dividends don't cover a $600 decline in value but they aren't far off. I wouldn't mind if I almost broke even on my TSMC shares with dividends. |

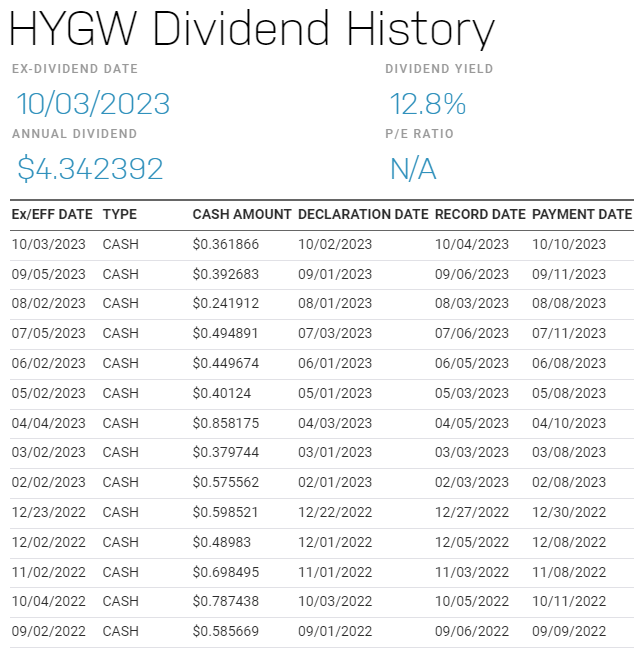

Others

|

|

Source. A corporate bond buy-write ETF, trades in the mid-$30s. |

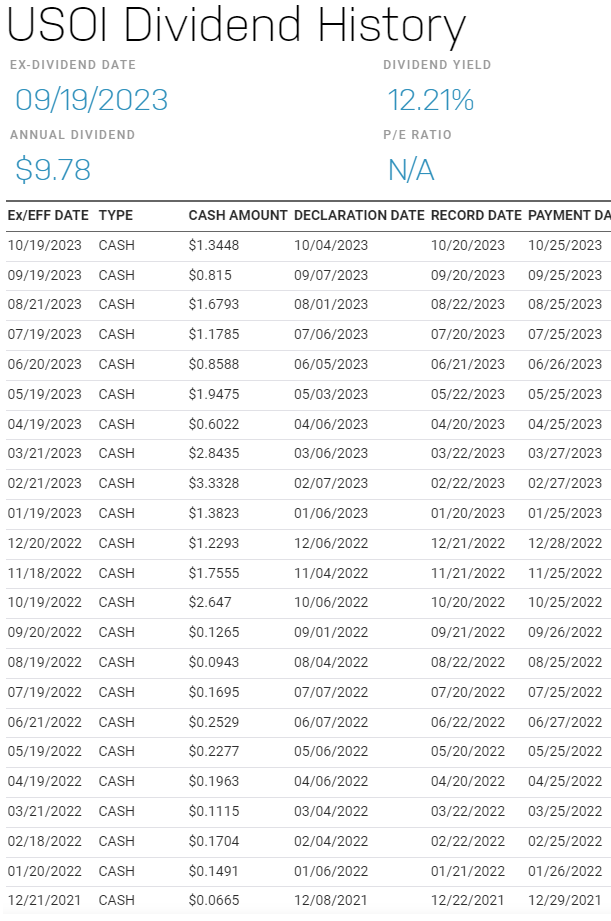

|

|

Source. An oil buy-write ETN, trades in the mid-$80s. For ETN caveats, check out the USOI and Barclay's OIL ETN tickers in March of 2020. |

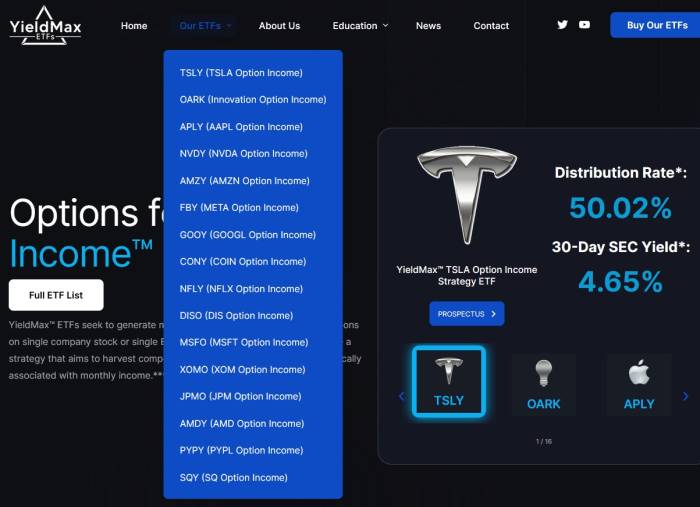

It's becoming a trend? There are new ETFs for Tesla and Apple and Netflix. QYLD tracks the Nasdaq 100 and PBP tracks SPX.

|

etrade |

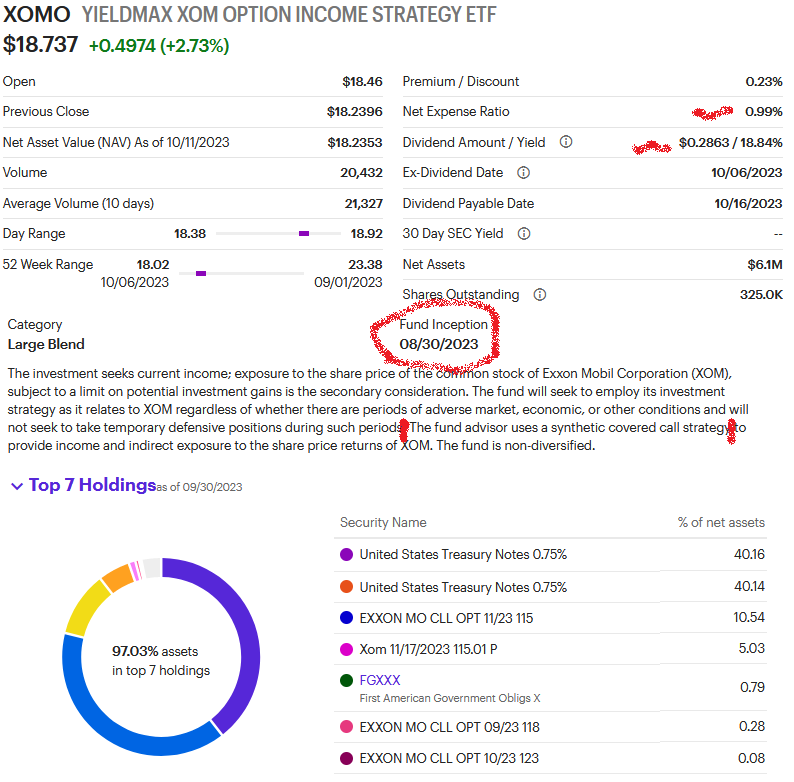

The investment seeks current income; exposure to the share price of the common stock of Exxon Mobil Corporation (XOM), subject to a limit on potential investment gains is the secondary consideration. The fund will seek to employ its investment strategy as it relates to XOM regardless of whether there are periods of adverse market, economic, or other conditions and will not seek to take temporary defensive positions during such periods. The fund advisor uses a synthetic covered call strategy to provide income and indirect exposure to the share price returns of XOM. The fund is non-diversified.

|

While the name is rather descriptive, I looked up the formal meaning of '

synthetic covered call':

|

Steady Options |

A synthetic covered call is an options position equivalent to the covered call strategy (sold call options over an owned stock). It consists of a sold put option.

Synthetic options strategies use bought and sold call and put options to mirror the payoff, risks, and rewards of another strategy, often to reduce complexity or capital requirements.

For example, suppose a stock, ABC, is trading at $100. Buying 1000 shares would be expensive ($100,000 or perhaps $50,000 on margin).

The same risk and rewards can be achieved by buying an at the money call option (strike price 100) and, simultaneously, selling an at the month put option (exercise price 100).

|

I guess this is why 80% of XOMO is in tnotes.

Outlook

It's hard to be confident about any new financial product, though at least TLTW has been around for more than a year.

I like the idea of setting a portion of my portfolio on autopilot theta gang and it's an even better option for my 401k where I can't sell calls/puts.

Some posts from this site with similar content.

(and some select mainstream web). I haven't personally looked at them or checked them for quality, decency, or sanity. None of these links are promoted, sponsored, or affiliated with this site. For more information, see

.

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/08/bg3_guardian.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/07/warrior.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/07/web.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2019/01/viscera_cleanup_mop.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/07/_CRR3746.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/02/far_cry_view_00.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/05/squadrons_awing.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2017/05/dying_light_stadium.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/08/iwate_governor_ending.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2020/09/da_bears.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/08/bg3_character_creation.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2016/04/division_helo_00.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2023/08/monster_train_torch.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/11/deezer.jpg){kind=link}

{kind=link}

{kind=link}

Comments