In this post:

construction, code, and catching falling knives.

Doors and siding

The door is done. The cinder block is in place.

I probably need to take care of the wall before getting turf put in.

But even more important is protecting what's been done. I power washed and hit everything with deck sealer.

Using the paint sprayer for that structure was a must. Happily,

the sealer is clear and didn't make the connector hardware look all funky. On the other hand, the wood still looks rigid and dry where I was hoping for a nice, UV-blocking lamination. I'm not entirely certain any wood-protecting products can stand the SD sun, that certainly was the case with the

pre-Trex deck.

The project

left me with more than a few pieces of 1x6 and 2x2. Since the

pumphouse wall was just plywood, I nailed the wood pieces on, shiplap-style. It looks good and recoups $345 of redwood that would otherwise be scrap.

Graphics code

|

|

Source. Sobel edge filter on one of those canonical graphics processing images. |

I haven't written any

graphics processing code lately but

I found some neat stuff on github. The projects I looked at are largely paths I've already gone down, but it's nice to see what other coders are doing.

Bresenham vector rasterizer

Example code, click through for the whole thing:

void plotQuadBezierSeg(int x0, int y0, int x1, int y1, int x2, int y2)

{ /* plot a limited quadratic Bezier segment */

int sx = x2-x1, sy = y2-y1;

long xx = x0-x1, yy = y0-y1, xy; /* relative values for checks */

double dx, dy, err, cur = xx*sy-yy*sx; /* curvature */

assert(xx*sx <= 0 && yy*sy <= 0);

A clean graphics library

|

|

From the author: This library collects various image processing algorithms and provides simple access to them. All algorithms are implemented in Java and runs without any other dependencies. Some algorithms are pretty standard and others maybe do you know from Photoshop. Github link. |

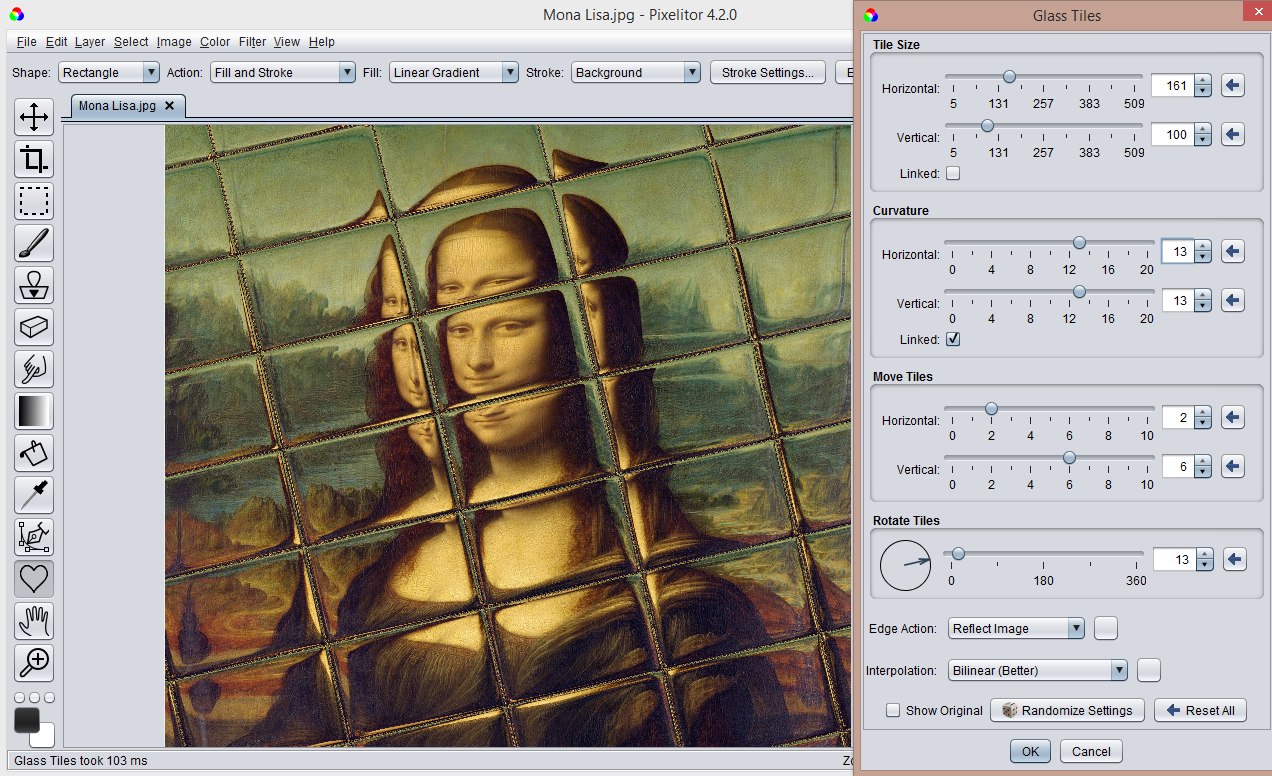

A library with a gui

|

|

Source. From the author: This is the source code of Pixelitor - an advanced Java image editor with layers, layer masks, text layers, 110+ image filters and color adjustments, multiple undo etc. Github link. |

Bear talk

Okay

so why did the lead image include Margot Robbie taking a bubble bath? First off, go watch The Big Short. Okay, now that you did, I don't have to tell you that Margot Robbie in a bubble bath is how the film explains subprime mortgages.

Borrowing against your port

I was reading

a WSB doompost about the (supposed) next subprime meltdown. I wasn't convinced, but I found the discussion and related material to be educational. The main theme of the post:

investments secured by a stock portfolio. You might have seen this:

Yahoo Finance

Yahoo Finance |

The Bloomberg index estimates that [Elon Musk has] already borrowed about $20 billion against his shares, leaving about $35 billion remaining that he could theoretically take out against the two holdings.

|

Elon borrows against Tesla and SpaceX shares to maintain his voting control while paying very little in taxes. See also: the recent "wealth tax" political football. Sort of a tangent but in defense of the Elizabeth Warren camp:

|

University of Southern California |

[Professor Ed] McCaffery came up with "Buy, borrow, die" in the mid-1990s to help students understand how the wealthy avoid paying taxes.

"The public thinks the rich get away with paying no taxes because they have expensive lawyers and accountants that regular people can't get who are working their magic," McCaffery said. "That's not the case. The rich aren't paying taxes because of perfectly legal reasons."

Here's how:

- Buy: An asset that will increase in value without producing income.

- Borrow: Money to live off based on this appreciating asset.

- Die: Avoid the 20% capital gains tax for selling an asset by holding the asset until death, when the asset can be sold off tax free by children or spouses.

|

Borrowing like a 1%er

I think

the most specific term for this is "margin borrowing". There are a few similar concepts that are important to be wary of when looking at data:

- "Margin debt" is often reported as an statistic measuring the aggregate health of investment portfolios. As I understand it, this value has historically been dominated by margin investing rather than margin loans/lines of credit.

- "Personal line of credit" also might describe borrowing against your equity holdings, but the traditional PLCs have used property or vehicles to secure the debt.

- "Asset-backed loan" is like a PLOC for a business and may or may not use investments as collateral. Of course, these days closely-held corporations used for tax avoidance aren't uncommon.

But how common are margin loans/lines of credit for people with a net worth in the mere 6-7 digits? If it's just Elon and Bezos, there really isn't a need to break out the dancing bears video.

To the doompost

As you might imagine,

the post starts with a callback to 2008 because all WSBers worship The Big Short and MJB.

catbulliesdog catbulliesdog |

There is not a repeat of the 2008 sub-prime debacle with NINJA (No Income, No Job, no Assets) loans. What is new - and whenever you get a financial crisis it's always, ALWAYS driven in large part by a "new" type of financial instrument (read debt) - is the sheer number of homes being bought up by with cash, and it's inferred these are all institutions and foreigners. For example, about $90 billion in US real estate was bought by foreigners in 2021. Wall Street however, blew that away, hitting as high as 1-in-7 of all homes and 1-in-2 of all apartments.

Now, people look at that record institutional/foreigner buying and think it's the explanation, but the truth is, even with those crazy numbers, 6-in-7 homes and 1-in-2 apartments are still being bought by regular people, often with, again, "cash".

These purchases are frequently referred to as "cash buys" because the buyer just pays the seller cash. However, they don't actually have piles of cash lying around in freighters to pay for this stuff. They take out loans. Specifically, they take out loans on their equity assets.

|

If you know anyone buying or selling a house,

you know that everyone's offering cash and/or 5-10% above asking. If these loans are secured by an investment portfolio rather than the house itself, it helps explain this phenomenon.

|

/u/Oddestmix

Someone clarify if I understand this correctly: he is saying that people are leveraging their portfolios to make "cash" deals? When equities go down and margin is called, people will have to liquidate the homes to cover margin?

|

|

|

/u/filstolealan

Most "cash" purchases by richer folks in the DC area are actually being structured as loans against brokerage accounts. Never seen it until covid. now its pretty standard

|

|

|

|

/u/champ999

How does this work, you go to the bank and say "here's my vanguard account with 5 million, give me a loan for a 2 million dollar house"? And since you have assets they give you a low interest rate since it's safe?

I guess I don't understand how to a seller it's cash that way as opposed to a traditional home loan.

|

|

|

|

|

/u/Overhaul2977

It is governed under Regulation U. The most a bank can loan is for 50% of the stock?s value. If the value falls, the person who took out the loan needs to cure the shortfall or the stocks are sold to help cure it. The borrower is still on the hook for any shortfall.

It is the primary cause for the crash of 1929, but the 50% limit did not exist back then so the damage should not be nearly as pronounced today.

These are also on the Fed?s radar. You?re required to register with the Fed if you make margin loans using securities as collateral.

|

I looked up some stats, last year all-cash home purchases were around 30%. Since 2000, this number that has fluctuated between 21% (cough, 2006) and 34% 2012. So

the cash purchase phenomenon isn't unheard of, but similar to a time when home values had collapsed and lenders were extremely wary.

It should be said, of course, that median price per square foot has almost doubled since 2000, meaning the cash purchase is a heavier lift than in 2012. The question I haven't found an answer to:

how many of these cash purchases are secured by a margin loan? There's certainly a risk that a market pullback would trigger a series of margin calls on the "new finiancial instrument" used to obtain these overpriced properties.

Burry to Xi

|

catbulliesdog |

So basically, we've got loans on inflated assets fueling loans on other inflated assets. This is feedback loop that goes parabolic.. then crashes, hard.

|

WSB has a steady trickle of doomposts that hit #1 on the front page. They always warn of

global financial disaster caused by a *hand wave* positive feedback loop implied by their text wall. Perhaps on purpose, these posts often pivot from the mechanism of catastrophe to something more concrete but less dire. To whit:

|

catbulliesdog |

But the coming death spiral of equity/asset sales isn't the only giant elephant in the room everyone is ignoring. I'm talking of course, about Evergrande in specific and Chinese property bonds in general.

|

I'm not sure developer defaults in China will matter if margin borrowing "goes parabolic". I won't fault OP for stream of consciousness, but it's important to recognize that the margin-secured real estate catastrophe argument kind of just ends.

But let's talk Evergrande

Evergrande has been defaulting for a few months now, what's new there? If OP is throwing shit at the wall, this could be what sticks.

|

catbulliesdog |

Evergrande hasn't made hundreds of millions of dollars of interest payment on bonds since September. A couple weeks ago they failed to pay the principal payment on a maturing bond to the tune of $2.1 Billion. So, you'd think that means their debt is junk and they've defaulted, right?

Not so fast. Let's check what the big 3 ratings agencies have to say about it:

Fitch: RD - Restricted Default

S&P: SD - Selective Default

Moody's: Caa1- Rated as Poor Quality and Very High Credit Risk

The reason Wall Street can survive a hit to something like AMZN and the indexes is that they're hedged to the balls for stuff like that. Know what they're not hedged for? Chinese property bonds universally going to zero.

|

Cue

the Big Short scene where Steve Carell's character has a chat with Standard and Poor's.

I don't really know enough about ratings to say whether OP is correctly outraged or if "selective default" is a finance way of saying "gtfo". I'm committed the Big Short theme so I kinda got to leave this in even if I have nothing interesting to say about it.

"Know what they're not hedged for? Chinese property bonds universally going to zero." Big, if tru.

Evergrande unwinding the global economy would require a lot of Wall Street incompetence and Beijing complacence to be catastrophic, but with some stats I could see some impact to whoever has significant exposure to Chinese property developers.

Zillow

OP then meanders back to the US real estate bubble to talk about

a different kind of all-cash buyer:

|

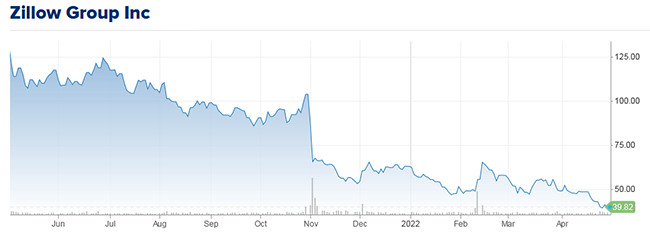

catbulliesdog |

We actually got a brief preview of what this is going to look like thanks to the wild incompetence and greed at Zillow - Z. Their stock crashed 40% in five days when it was revealed they'd bought too many houses they couldn't rent or flip and had to sell them at a loss. And that was just a couple of neighborhoods in Arizona. When this hits nationwide, it's going to be exponentially worse.

|

The share price thing is a bit of a red herring - Zillow's share price should take a major hit for the company's unsuccessful adventure in home flipping. $Z is not a proxy for the US economy. But I think this is an important case study that relates back to

whether or not the margin loan phenomenon will trigger default dominos. In the Zillow case, they offloaded their inventory and survived. There was ample demand to prevent the feedback loop from going positive.

What will happen if margin-secured homeowners start getting margin called because of a market pullback? Their first safety net is that 50% rule and having diverse investments. Their second safety net is simply taking out a mortgage. Their third is selling.

The market and home values would have to suddenly tank for other market pressures to not prevent this from "going parabolic".

What about the Zillows and Black Rocks? Maybe insignificant? As OP says, "6-in-7 homes and 1-in-2 apartments are still being bought by regular people, often with, again, 'cash'".

|

|

Source. Will this subprime meltdown comic see new life? We certainly have a lot more zero-dot-line houses these days. |

Conclusion

Anyway, while

I'm not sure this will be the next financial crisis, I could totally picture Margot Robbie in a bubble bath five years from now explaining what margin borrowing is.

<3

Some posts from this site with similar content.

(and some select mainstream web). I haven't personally looked at them or checked them for quality, decency, or sanity. None of these links are promoted, sponsored, or affiliated with this site. For more information, see

.

![[+]](https://www.chrisritchie.org/kilroy/archive/2022/03/reddit_forte11_chat.png){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/07/warrior.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2022/05/search_impressions.png){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2019/01/viscera_cleanup_mop.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2022/05/autogen_page.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/02/far_cry_view_00.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2022/05/zillow.png){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2017/05/dying_light_stadium.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2022/05/nn_for_babies.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2016/04/division_helo_00.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2022/05/food.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2015/11/deezer.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2022/05/photography_lesson.jpg){kind=link}

![[+]](https://www.chrisritchie.org/kilroy/archive/2016/08/witches_lair.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}